As C# is a strongly typed language, it is necessary to specify data types when declaring variables and class properties in cBots, indicators, and plugins. In contrast, Python is dynamically typed, so variable types are inferred automatically. However, when developing cBots using the cTrader API, the same conceptual types are preserved for consistency between both languages.

cTrader Algo API does not allow all data types to be used as customisable parameters, and this is why it is essential for algorithm developers to understand and navigate across the supported types carefully.

Note

Python cBots, indicators and plugins use customisable parameters declared in their .cs files.

Parameter use cases and UI

cTrader supports only these parameter types with the key use cases and related UI elements reflected in the table below.

C#

Python

Use cases

UI element

int

int

Order volume, number of bars, number of periods, etc.

Number input field (with stepper)

double

float

Price value, order volume, etc.

Number input field (with stepper)

string

str

Custom message, position label, etc.

Text input field

bool

bool

Protection mechanisms, allow trading, allow email, etc.

Dropdown yes/no

DataSeries

api.DataSeries

Source of market prices, etc.

Dropdown list

TimeFrame

api.TimeFrame

Chosen time frame, etc.

Period selector

enum

Enum

Chart drawings alignment, individual risk levels, etc.

Dropdown list

Color

Color

Chart drawings, colour of technical analysis means, custom elements, etc.

Colour picker

DateTime

DateTime

Getting strongly typed date and time in the algo time zone

Date and time picker

DateOnly

DateOnly

Getting strongly typed date

Date picker

TimeSpan

TimeSpan

Getting strongly typed time interval or time of the day

Time picker

Symbol

Symbol

Getting strongly typed single symbol

Symbol picker

Symbol[]

Symbol[]

Getting strongly typed multiple symbols in an array

Multi-symbol picker

Enum[]

Enum[]

Getting strongly typed multiple values of an Enum type in an array

Multi-enum value picker

TimeFrame[]

TimeFrame[]

Getting strongly typed multiple TimeFrame values in an array

Multi-period picker

Warning

You may not be able to use some of the parameter types above if you are using an older version of cTrader or Algo API.

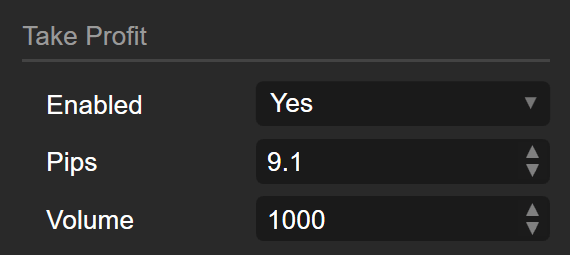

For example, the cTrader UI reflects C#'s bool, double, int and Python's bool, float, int types as follows.

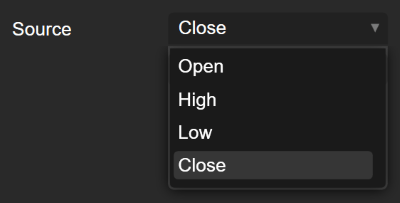

The next three examples show C#'s DataSeries, custom enum, string and Python's api.DataSeries, Enum, str data types (for which we also provide the full code in this guide).

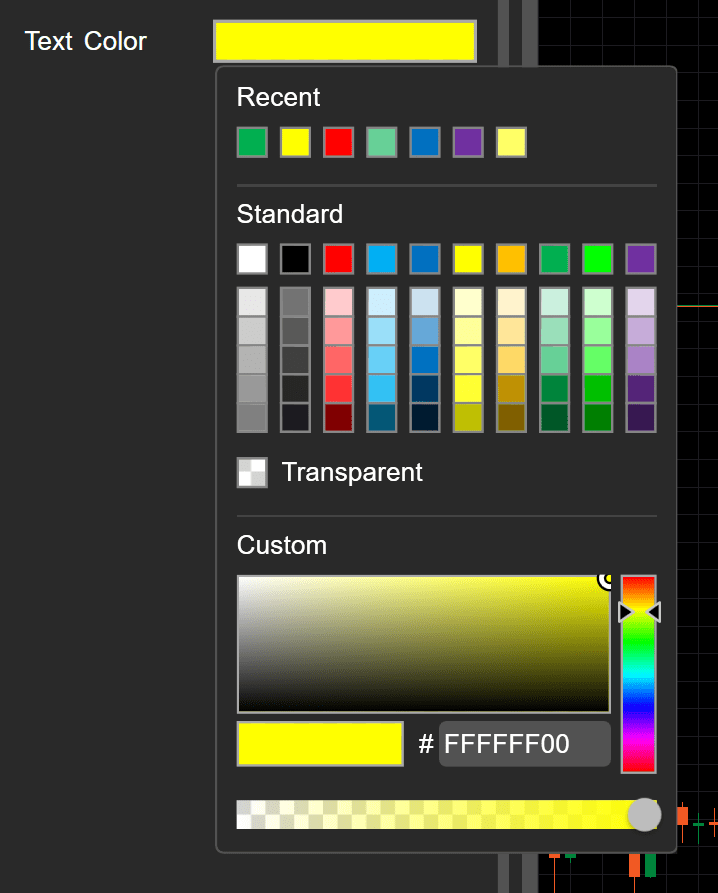

As shown below, C#'s Color and Python's Color parameter type is represented by a colour picker.

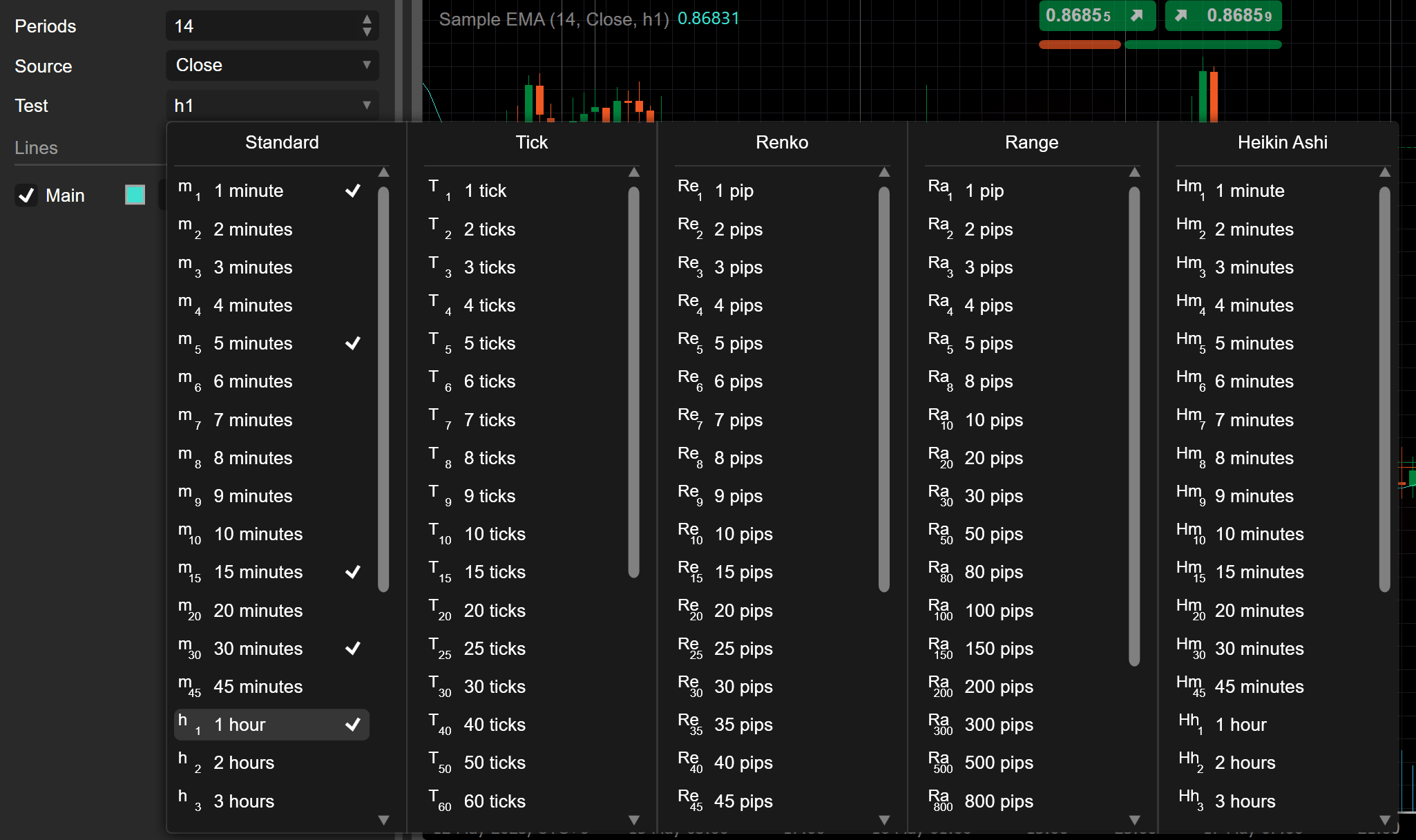

Finally, the UI of C#'s TimeFrame and Python's api.TimeFrame data mirrors the period options available in trading charts within the Trade application.

cBot examples

The position label is a C#'s string and Python's str parameter in the following cBot.

In the example below, C#'s double and Python's float data type serves as a parameter to input the order volume in lots. The cBot executes a buy market order after three consecutive red bars.

usingSystem;usingSystem.Collections.Generic;usingSystem.Linq;usingSystem.Text;usingcAlgo.API;usingcAlgo.API.Collections;usingcAlgo.API.Indicators;usingcAlgo.API.Internals;namespacecAlgo{[Indicator(AccessRights = AccessRights.None)]publicclassNewIndicator4:Indicator{privateBars_hourlyTimeFrameBars;privateBars_targetTimeFrameBars;[Parameter("Chosen Time Frame")]publicTimeFrameTargetTimeFrame{get;set;}[Output("Main")]publicIndicatorDataSeriesResult{get;set;}protectedoverridevoidInitialize(){_hourlyTimeFrameBars=MarketData.GetBars(TimeFrame.Hour);_targetTimeFrameBars=MarketData.GetBars(TargetTimeFrame);}publicoverridevoidCalculate(intindex){Result[index]=_hourlyTimeFrameBars.HighPrices[index]-_targetTimeFrameBars.HighPrices[index];}}}

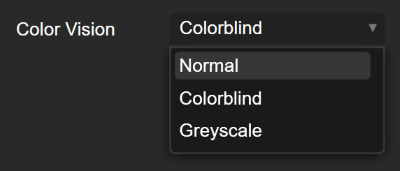

There is a playful (colour-blind test) indicator that offers enum colour vision options (for example, normal, colour-blind, and greyscale) for users to determine the colour of a horizontal line drawn on the chart.

To summarise, by choosing the correct data type for the declared variables and class properties, you will be able to create cBots and indicators that can handle even non-standard tasks.